State of the Industry 2017: Dairy exports have a positive outlook

With a ‘pretty good’ outlook for global demand, the U.S. dairy export sector could earn the title of MOST LIKELY TO TAKE OVER THE WORLD.

Largest US Dairy Export Destinations

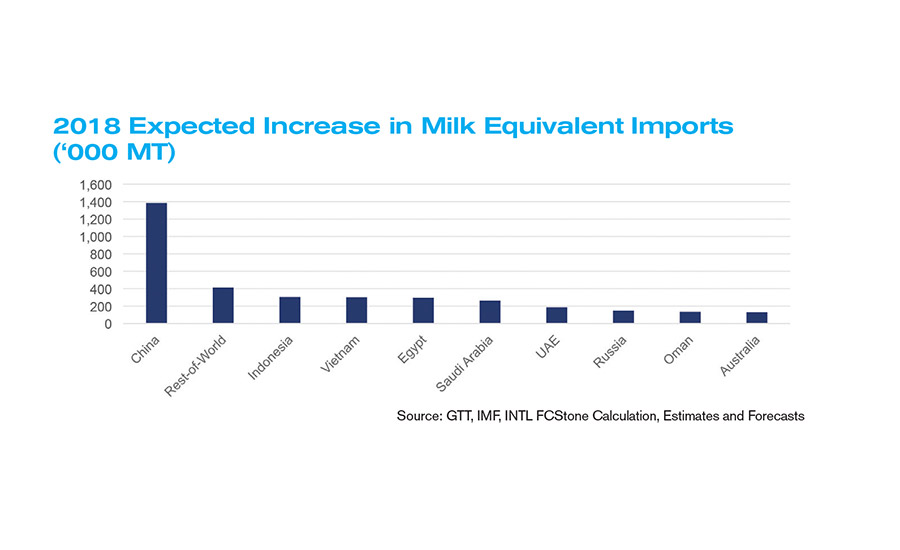

2018 Expected Increase in Milk Equivalent Imports

Don’t get distracted by the headlines in 2018. The renegotiations of the North American Free Trade Agreement and the U.S.-Korea free trade agreement will demand a lot of attention, but assuming neither of them is wiped off the board completely, growing milk supplies in the other major exporting countries will create the headwind for U.S. exports.

Milk | Cheese | Cultured | Ice Cream | Butter | Non-dairy Beverages | Ingredients | Exports

During the second half of 2017, farm-gate margins in Europe, New Zealand and Australia have moved back to profitable or very profitable levels, and that will drive an expanding milk supply globally in early 2018 and increased competition in the export market.

Dairy exports showing promise

Obviously free trade agreements (FTAs) do have an impact on trade flows by changing the relative competitiveness of suppliers, but a threat to change an FTA does not change the short-term competitiveness of suppliers. Anyone who bet on a drop in U.S. exports to Mexico in light of Donald Trump’s election victory was wrong.

January to July, U.S. exports of nonfat dry milk/skim milk powder and cheese exports to Mexico were record-setting, with total milk equivalent exports up 16.4% from the first seven months of 2016. While aggravating or insulting your trade partner doesn’t help exports, until there is a change in the underlying economic incentives, political banter probably won’t have a big impact on U.S. dairy exports in 2018.

Overall, our global demand outlook for 2018 is pretty good. We track imports into more than 250 destinations and model import demand for the top 31 countries that make up about 85% of global imports, then roll the other 220-plus destinations into a Rest-of-World group and model them together. The models are driven by population, real GDP growth, dairy prices and other country-specific variables like oil prices for large oil-exporting countries.

Out of the top 31 dairy importers, the International Monetary Fund (IMF) is forecasting positive real economic growth in 2018 for 28 of them. Real GDP growth in both Japan and Brazil are forecast down just a fraction of a percent in 2018, which isn’t great for dairy imports, but it’s not a big cause for concern.

Real GDP for Venezuela is forecast down 4.5%, which is looking too optimistic at this point. Sadly, Venezuela has fallen from being sixth largest importer in 2012 to the 116th largest year to date in 2017, importing a little less than Barbados. So a further decline in economic conditions within Venezuela likely won’t have much impact on global dairy demand in 2018.

China drives demand growth

Where will the demand growth be in 2018? China. Always China. The answer to nearly every global dairy demand question is China. We’re not expecting a repeat of the 2013/2014 import surge; in fact, we’re forecasting Chinese import growth to slow from about 18% in 2017 to 10.5% in 2018. But China imports almost three times more than the second-largest importer (Mexico). With that much volume, it takes only small percentage changes to drive large changes in tonnage.

For instance, we’re forecasting a 15.7% increase in imports for Vietnam, but that is an increase of only 301,000 metric tons (MT) of milk. The 10.5% increase for China absorbs an additional 1,383,000 MT of milk. In addition to China and Vietnam, we see the strongest volume gains for Indonesia, Egypt and the 220-plus smaller importers we call “Rest-of-World.”

So good growth in global demand, but how much volume will the United States get? China, Vietnam, Indonesia and the rest of the world are already in the top 10 export destinations for the United States, so U.S. exports stand to benefit from the expected import bounce in those countries. But the Middle East makes up only a small portion of U.S. exports, and Europe/Oceania will likely benefit most from a rebound in Middle East demand.

Mexico’s impact

The biggest export market for the United States is Mexico, taking about 27% of U.S. milk solids exports the past 12 months, so obviously Mexican import demand will have a big impact on U.S. exports. Mexico’s imports from all sources that we track were up 10.7% on a milk-equivalent basis in 2016, and they are up 13.7% for the first seven months of 2017.

Mexican imports have been larger than expected the past 18 months, and given the election in mid-2018, they could stay strong for the first half of the year too. But domestic milk production is growing (up 2.2% January-August), and per-capita availability has shot way above the long-run relationship to GDP, dairy prices and oil prices, so it wouldn’t be too surprising to see a slowdown in Mexican imports at some point in 2018.

We’re forecasting global imports to be up 6.0% on a milk-equivalent basis in 2018, with U.S. exports up 7.2%. To do that, the United States is going to have to stay price-competitive on nonfat dry milk/skim milk powder, cheese and whey products. In mid-2017, the United States is sitting on record stocks of cheese, dry whey, high-protein whey protein concentrate, whey protein isolate and lactose.

The United States can get competitive and get the product offshore, or can expect new record high stocks in 2018, too. With production likely growing in all of the other major exporting countries, they are going to be boosting exports as well. So the volume of exports will be up, but the value of exports might be close to steady or down as prices will be under pressure.

Milk | Cheese | Cultured | Ice Cream | Butter | Non-dairy Beverages | Ingredients | Exports

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!